Most of the electric vehicles (EVs) on Canada's road are manufactured outside Canada. Stellantis, General Motors, and Toyota manufacture a few battery-electric vehicles (BEVs) and plug-in hybrid-electric vehicles (PHEVs) at thair plants in Ontario, but most vehicles arrive from around the world. The diagrams below illustrate where these vehicles come from, and what trends are emerging. During 2025 purchase incentives were halted both federally and in some provinces, and the carbon tax on motor fuels was abolished in April 2025. Predictably, sales plunged. EV sales have now started to recover, and In April 2026 the federal government lauched its new Electric Vehicle Affordability Program (EVAP) with rebates up to $5,000 during the first year. Incentives will drop every year through 2030.

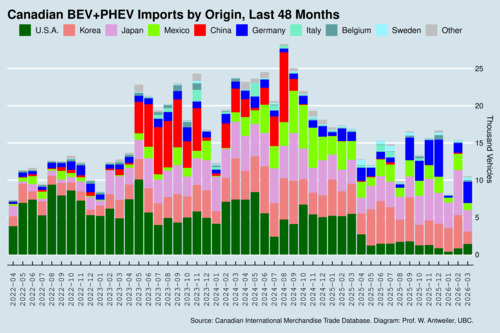

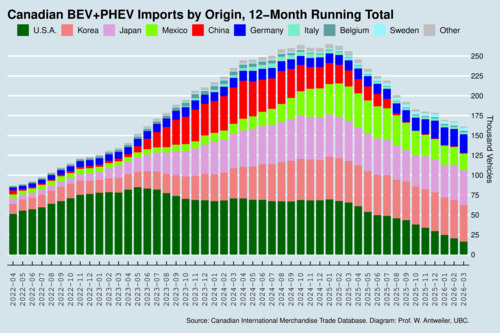

Data from Canada's International Merchandise Trade database provides insights into the composition of EV imports. The first two diagrams show the total number of vehicles imported into Canada by origin country, where BEV and PHEV imports are aggregated. The first chart shows the monthly raw figures, which show some volatility. The second chart shows a 12-month rolling total, which smoothes the data and reveals trends more clearly.

click on image for high-resolution PDF version

There are two things that stand out very clearly in the diagram above. First, Chinese-made electric vehicles (mostly Teslas and Polestars) started arriving in Canada in earnest in May 2023. Imports from China collapsed completely after Canada's federal government imposed a 100% surtax on Chinese-made electric vehicles on October 1, 2024, following a similar move in the United States, and on top an existing 6.1% import tariff. Second, since April 2025, imports of US-made electric vehicles have dropped precipitously. Part of that was simply the effect or the removal of purchase incentives. Another contributor was a backlash against Tesla because of the political antics of its CEO Elon Musk. But the U.S. is also losing ground as the current government in the United States is openly hostile to electric vehicle adoption, and car manufacturers have been pulling back.

The Big Three car manufacturers produce several of its EV lines in Mexico, such as the Ford Mustang Mach-E, the Chevrolet Equinox and Blazer EVs, and the Honda Prologue. Mexico, as part of the Canada-US-Mexico Agreement (CUSMA) free trade area, has a competitive advantage.

click on image for high-resolution PDF version

Annual imports of EVs peaked during 2024. The chart above shows the rolling 12-month total, and some of the larger trends appear more clearly. The U.S. share is clearly declining, while the share of EV imports from Korea and Japan have risen significantly, followed by Mexico and Germany. Chinese EV imports have vanished because of the surtax. However, with the new order amending the Import Control List, as of March 1, 2026 there is new 49,000 annual quota for imports from China, and this quota will increase 6.5% per year. Part of the quota is reserved for low-cost vehicles with free-on-board price of $35,000. This share will rise from 10% in year 2 to 50% in year 5 of the program. The 6.1% base tariff will remain. As the chart shows, at its peak there were about 50,000 vehicles imported from China. The quota essentially restarts the sales volume that China had before the imposition of the surtax.

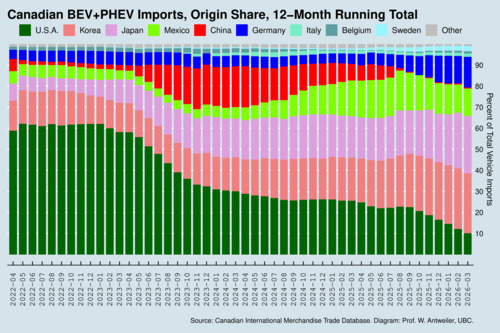

The next chart shows the running total expressed as percentage market shares. This diagram gives perhaps a better perspective on the compositional changes over time.

click on image for high-resolution PDF version

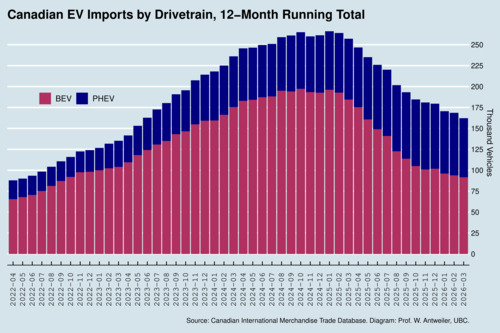

Another major trend that is visible in the import data is the increasing relevance of plug-in hybrid vehicles (PHEVs). The following diagram shows the number of imported BEVs and PHEVs.

click on image for high-resolution PDF version

What is most visible in the diagram is the increasing importance of plug-in hybrids. A major factor is that PHEVs tend to be cheaper than BEVs, and are thus able to reach larger segment of the automotive market. As choice is expanding, especially from Korean and Japanese manufacturers, the share of PHEVs is evolving. PHEVs have trade-offs. They have two types of engines, but a smaller electric battery. As large batteries are expensive, the cost of the gas engine is still keeping these vehicles cheaper than BEVs. But this gap may be shrinking, as the next diagram shows. But PHEV drivers will not face range anxiety, and even the small battery allows many PHEV users to drive on electricity almost all of the time, especially in urban areas.

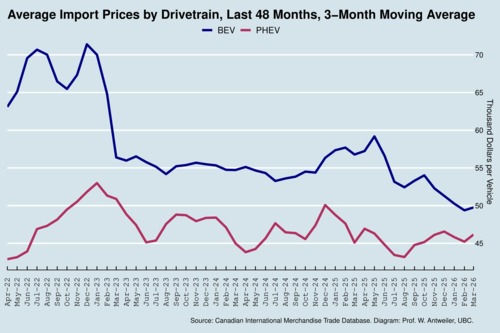

click on image for high-resolution PDF version

The last chart shows the price dynamics, separate for the two drivetrains (BEV and PHEVs). To smooth out monthly fluctuations, the prices are shown as trailing 3-month averages. There is a consistent price gap between BEVs and PHEVs of roughly $15,000. However, during late 2025 and early 2026 this gap has started shrinking as the average cost of imported BEVs is falling (while the cost for PHEVs is holding steady). By March 2026, the gap had shrunk to barely $5,000. What is driving this is in part the composition. Currently, the lowest cost EVs arrive from Korea and Japan, and increasingly Mexico. There seem to be fewer buyers of expensive US-made EVs. As more affordable (and somewhat smaller) BEVs are entering Canada's automotive market, that is good news for increased EV adoption in Canada.