As oil shocks come, 2026 may become the biggest one yet in history — bigger than the energy crisis in 2022 caused by Russia's invasion of Ukraine, and larger than the 1973 oil crisis and the 1979 oil crisis. Crude oil prices have crept up to over $100/barrel for the Brent type, and they may have to rise further as the conflict in the Middle East continues. How bad will it get? The Economist magazine described today's situation as oil markets are still in La La Land. I find myself in agreement with that sentiment: it may indeed get worse before it gets better.

click on image for high-resolution PDF version

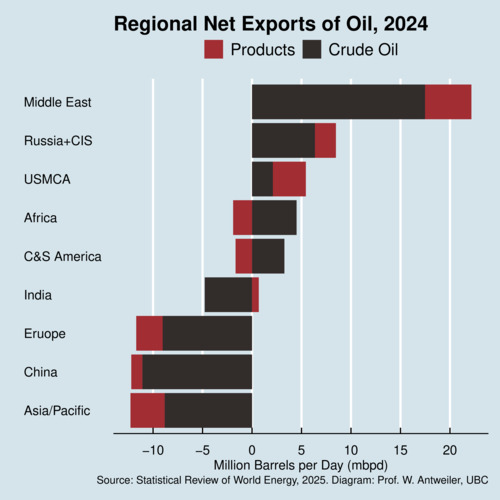

As the above diagram for 2024 shows, the world remains rather dependent on the Middle East for its oil output, but not only for crude oil, but also for refined oil products and oil derivatives such as naphtha. And refined products are more difficult to replace because there is not enough refining capacity to make up. The oil supply chain isn't just about getting crude oil to foreign markets, but also about refined products. The other major supplier of refined products is the United States, and they are running at capacity. Overall, North America is self-reliant when it comes to oil, but Europe, China, and the Asia-Pacific region are not so fortunate. This is where the physical crunch will be felt first. Already refineries in Asia have cut back on output for lack of crude supply, stockpiles of refined products such as diesel and kerosene are dwindling fast, and the prices for refined products have risen much more than for crude oil.

How bad it gets depends on the duration of the conflict. The longer it lasts, the deeper and the more sustained the effects. Economic analysis suggests that there are four distinct levels of repercussions.

First is the macro-economic effect from higher oil prices, which will dampen demand for everything else as consumers and businesses adjust their expenditures. This is the shift in relative prices in the economy. And things can get worse. The oil market needs to find a new equilibrium price level, and that new level can only be much higher than today once stockpiles have been used up. Today the effect remains significantly cushioned. Prices well above $150/barrel are conceivable. Higher crude prices get passed on to consumers directly through fuel purchases, and somewhat slower, indirectly through buying goods that depend on transportation services.

‘Some countries will turn to rationing, others to export controls.’

Second is the effect of the missing physical quantity of oil, the actual shortage. This shortage will be asymmetric regionally and across different products. As the chart above shows, some regions are simply more vulnerable than others, and the net-exporter regions may constrain exports to protect their own domestic markets. This in turn dampens the effect in the net-exporter regions and aggravates the effect in the net-importer regions. If the situation worsens, countries will look out for themselves first and institute export controls. Shortages may entail rationing in some countries. Some goods will not get delivered, or delivered late, leading to inventory shortages and production curtailments. Shortages will also differ across fuel products, with aviation fuel being affected significantly more than gasoline. Refineries cannot produce an arbitrary mix of fuel types as their relative shares are determined by the nature of the distillation process. Physical shortages require offsetting reductions in demand. airlines have already been cutting back short-haul flights in Europe. Some Asian countries are trying to reduce energy demand with various measures.

‘The oil shock affects not only crude oil but also refined products and many by-products.’

The third effect is through oil byproducts. Missing crude oil means less refined products, and fewer byproducts. There are a number of important byproducts from oil refining. One such byproduct is sulfur, which is used in battery chemistry and for phosphorus production. Nearly half of world sulfur output sails from oil producers in the Middle East through the Strait of Hormuz. Fertilizers (urea and ammonia) are also affected, and lacking fertilizers spill over into reduced agricultural output. Roughly a third of the world's methanol production is also affected, and methanol is an important feedstock for plastics. That in turn affects many manufacturers (notably in China) that rely on such feedstocks. Even graphite feedstocks are affected, as graphite has become a key ingredient in battery manufacturing. Graphite is a byproduct of oil refining by converting petroleum coke residue into synthetic graphite at high temperatures. Cheap energy in the Middle East is also used to produce energy-intensive products, notably aluminum. The Middle East accounts for a little less than one-tenth of world output of aluminum. And then there is helium, a by-product that is separated from natural gas through cryogenic distillation.

The fourth effect is through the entire supply chain, because so many goods depend on "upstream" inputs that depend on oil directly or on energy. An oil shortage percolates eventually through the entire production system. Economists study these systemic repercussions with an input-output matrix of the economy. Fortunately, much of our modern economies are service-driven, but higher oil prices will make some products less affordable, and some services such as those in the hospitality industry that rely indirectly on transportation.

So what can we expect to happen next?

Futures prices for oil seem to suggest that a settlement in the conflict is not too distant in the future. At least the U.S. president seems eager to call it a day and wrap up some agreement, likely any agreement that allows him to come out on top—at least in the perception of his supporters. Iran, on the other hand, is pursuing a strategy of asymmetric endurance. The Islamic Revolutionary Guard Corps (IRGC) that has even more become the de-facto ruler of Iran knows that it can continue to inflict economic pain on its population for much longer than American voters are prepared to endure with rising gasoline prices. Their calculation is that the longer the negotiations drag on, the better the terms of an eventual deal. Meanwhile, the Strait of Hormuz will remain closed.

Even when the Strait of Hormuz opens up again, de-mining it and restarting production around the Gulf countries will take weeks and months during which world oil markets will remain under-supplied.

Frankly, I would be surprised if a deal between Iran and the United States is struck any time soon. I hope that I am mistaken, but the odds are not in favour of a world returning back to "normal" soon. With his ill-considered aerial bombing campaign, Mr. Trump let the genie out of the bottle and there is no way through which he can put it back in. There is no straight-forward military option to reopen the Strait of Hormuz. The Strait is easy to mine, and ships are easy to attack with cheap drones and missiles. Re-opening the Strait of Hormuz will require negotiations, and these will be neither quick nor easy.

‘Asymmetric endurance works to the advantage of Iran's regime in peace negotiations.’

There are now two main issues in this conflict: re-opening the Strait of Hormuz, and shutting down Iran's nuclear bomb program. These two issues are intertwined. While it may look conceivable to reach separate deals on the two issues, it is hard to see how to disentangle them. If the U.S. release the pressure on Iranian oil exports in a deal to re-open the Strait of Hormuz, Iran will have little incentive to reach a deal about its nuclear program. Iran has learned to put a thumb on the Strait of Hormuz, and they will use this thumb for maximum gain. But Iran does not have endless time either because Iran relies on shipping for 90% of its oil through the Strait, and they are losing the oil revenue that has propped up their economy. But the IRGC leaders believe that they can endure economic pain for many more months before their economy starts to shatter, prices soar, and people go hungry because of supply shortages. Iran's repressive regime has shown that it won't stop at shooting its own people to suppress protests. The conflict can drag on for many more weeks, even months. And a deal may well see Iran capturing revenue from transiting ships through the Strait of Hormuz, even if it contravenes international maritime law. Just don't expect a quick settlement. And if the Strait of Hormuz opens up again, transits may become more expensive.

‘Public policy should not lose focus on the energy transition.’

Lastly, let me address public policy in Canada and elsewhere. Reducing fuel taxes appears to provide relief, but that relief is largely cosmetic. The market still needs to find its new equilibrium, and that requires people conserving fuel. Providing tax relief stimulates demand, rather than suppress demand. Pushing against the market means that some of the tax relief will evaporate. While lowering fuel taxes is always popular, it is also rather ineffective. It may be smart politics (to take the wind out of the sail of opposition politicians), but it is not good policy—even if some of the revenue loss is offset by higher royalties or sales taxes. Instead, as economists would argue, stay away from messing with prices and instead focus on providing income relief to those most in need. The main lesson from the 2026 oil crisis is that we need to lessen our dependence on fossil fuels, and turn more towards clean electricity. Smart governments would see today's crisis as an opportunity and as an imperative to accelerate the energy transition.

Recent Blog Entries

- Should data centres provide demand flexibility to protect BC's electricity grid? (June 8)

- Wind power is growing in British Columbia (June 5)

- Canada needs better rail, but not high-speed rail (June 2)

- How are Canada's electric vehicle imports trending? (May 9)

- The 2026 oil shock may become larger than you think (April 30)

- Improving road safety and saving lives with Leading Pedestrian Intervals (April 2)

- Where are BC's LNG exports sailing to? (March 27)

- Driving electric has become much more beneficial (March 17)

- Today's ruling by the U.S. Supreme Court won't end Trump's trade wars (February 20)

- America's Federal Reserve must stay independent (January 13)

- What good are stablecoins? (19 Dec 25)

- Canada's alcohol imports have shifted (27 Nov 25)

Topics

Months

Subscribe to RSS feed ![]()